Chinese Car Sales in Europe 2026: The Definitive Market Revolution Report

As we navigate through the second quarter of 2026, the European automotive industry is witnessing a seismic shift that few predicted a decade ago. The “Chinese wave,” once a distant ripple, has become a dominant force, reshaping the competitive landscape from the fjords of Norway to the bustling streets of Madrid. This comprehensive report analyzes the unprecedented surge in Chinese car sales across Europe in 2026, exploring the technological, economic, and political factors driving this transformation.

To complement the full analysis below, the short video summarizes the key findings of this Chinese car sales in Europe 2026 report in a quick ten-slide format. It is the fastest way to grasp the headline numbers, the leading brands, and the technology trends before diving into the detailed sections.

With that overview in mind, the sections that follow break down the statistics, the shift toward local European production, the technology advantage, the standout brands of 2026, and what all of this means for buyers and the wider market heading toward 2030.

The Statistical Reality: Breaking Records in 2026

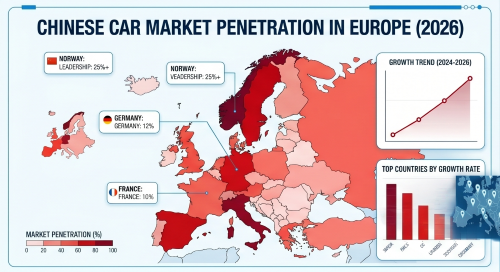

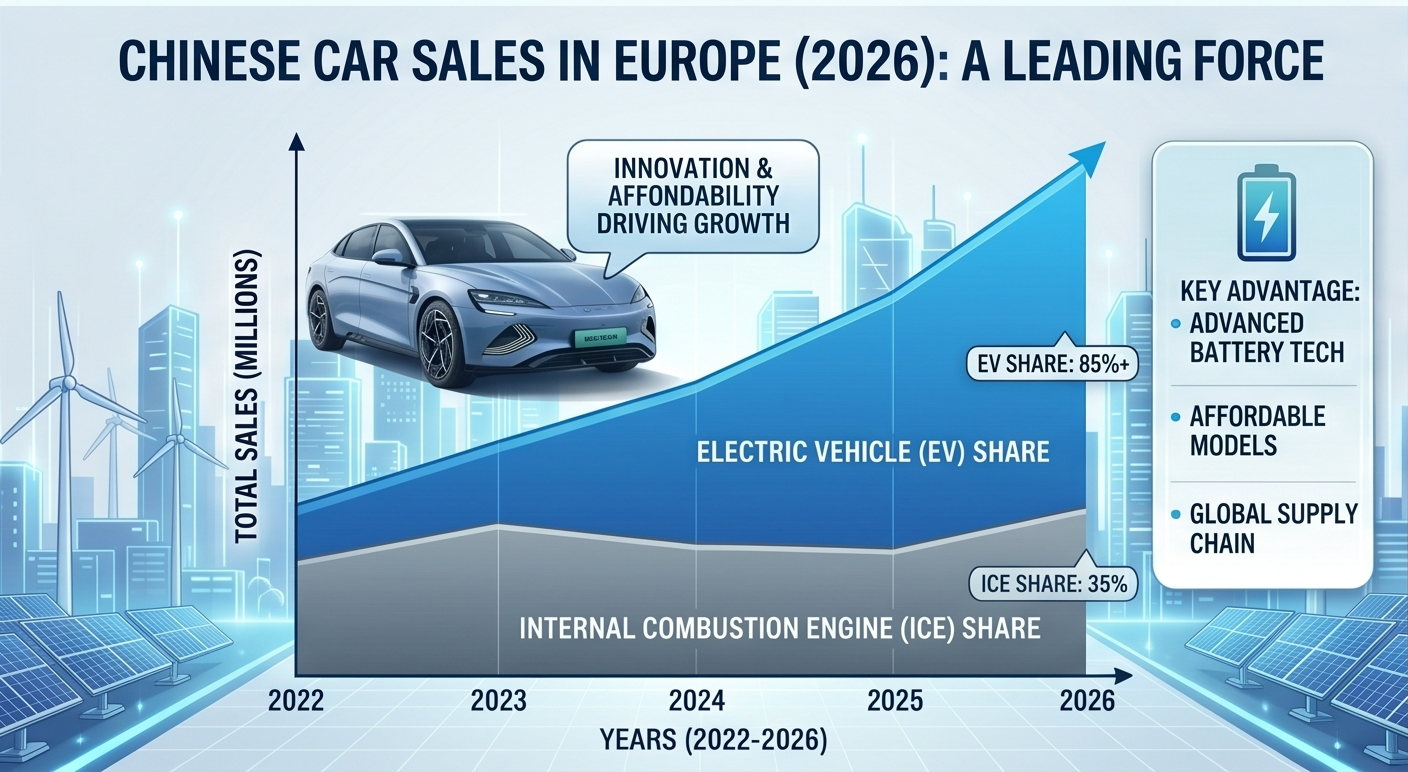

By the end of March 2026, data from the European Automobile Manufacturers’ Association (ACEA) revealed that Chinese-branded vehicles now command a 16.5% share of the total passenger car market in the EU. More impressively, in the Battery Electric Vehicle (BEV) segment, Chinese manufacturers have captured a staggering 31% of the market. This represents a 45% year-on-year increase compared to 2025, signaling that the initial consumer hesitation has been replaced by widespread acceptance.

The success is not limited to budget models. In 2026, high-end Chinese EVs are competing head-to-head with German luxury stalwarts. This shift is driven by a combination of aggressive pricing, shorter innovation cycles, and a superior grasp of software-defined vehicle (SDV) architecture. While European legacy brands struggle with legacy hardware and complex software integration, Chinese firms like BYD and NIO are delivering seamless, tech-first experiences that resonate with a younger, digital-native demographic.

Geopolitical Navigation: From Exporting to Local Production

A major narrative of 2026 is the strategic pivot of Chinese OEMs toward “Made in Europe.” Following the tariff discussions of previous years, the most successful brands have successfully localized their supply chains. The BYD plant in Szeged, Hungary, is now operating at 85% capacity, churning out models specifically tailored for European tastes. Similarly, Great Wall Motor (GWM) and Chery have established assembly hubs in Spain and Poland through joint ventures or brownfield investments.

This localization has two primary benefits: it immunizes these brands against fluctuating trade policies and significantly reduces the carbon footprint associated with long-distance shipping. In an era where the EU’s “Green Deal” and Carbon Border Adjustment Mechanism (CBAM) are in full effect, being a local producer is no longer an option—it is a survival requirement. The result in 2026 is a Chinese automotive sector that is deeply integrated into the European economic fabric, creating thousands of jobs and fostering local R&D partnerships.

Technological Leadership: Why European Consumers are Switching

1. Battery Innovation and Solid-State Breakthroughs

In 2026, the conversation has moved beyond “range anxiety” to “charging efficiency.” Chinese battery giants like CATL and BYD (FinDreams Battery) have introduced semi-solid-state batteries into production vehicles sold in Europe. These batteries offer 40% higher energy density than traditional lithium-ion packs, allowing for ranges exceeding 800km (WLTP) in mid-sized sedans. Furthermore, 800V high-voltage platforms are now standard in most Chinese EVs priced above €35,000, enabling a 10% to 80% charge in under 12 minutes.

2. The Software-Defined Vehicle Advantage

The 2026 models from XPeng, NIO, and Xiaomi have redefined the cockpit experience. European drivers are increasingly prioritizing infotainment, Over-the-Air updates, and autonomous driving features. Chinese brands have excelled in integrating AI assistants that actually work, alongside Level 2++ and Level 3 autonomous features that handle urban traffic with remarkable smoothness. The hardware is no longer the sole selling point; it is the ecosystem—an area where Chinese tech-automotive hybrids have a clear lead.

Brand Spotlight: The Winners of 2026

BYD: The Global Powerhouse

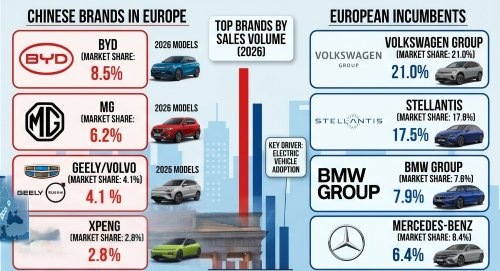

BYD has officially become a household name in Europe. With a diverse lineup ranging from the compact Dolphin to the ultra-luxury Yangwang U8, BYD covers multiple segments. Its 2026 success is largely attributed to vertical integration; by manufacturing batteries, semiconductors, and core EV components, BYD has avoided many of the supply challenges that continue to affect some rivals.

MG Motor: The Value Champion

MG continues to be the entry point for many Europeans transitioning to electric mobility. The MG4 and the newly released MG2, positioned as a sub-€20,000 electric city car, have dominated value-focused discussions in the UK, France, and Italy. By blending historic brand recognition with modern Chinese efficiency, MG has successfully bridged the gap between old-world loyalty and new-world technology.

Xiaomi Auto: The Disruptor

After the global success of the SU7, Xiaomi’s 2026 expansion into the European SUV market with the MX11 has attracted major attention. By leveraging its existing smartphone user base and retail network, Xiaomi has created a unique “Human-Car-Home” ecosystem that traditional automakers are still trying to match. Its cars are seen as fashion statements and lifestyle tools as much as they are transportation.

The Green Competition: Environmental Standards in 2026

The year 2026 coincided with the implementation of stricter Euro 7 emission standards for internal combustion engines and new life-cycle assessment rules for batteries. Chinese manufacturers were surprisingly well-prepared. Most 2026 Chinese models feature “Battery Passports,” documenting the origin of key materials such as cobalt and lithium. This transparency has helped challenge the narrative that Chinese EVs are less environmentally accountable than European counterparts.

Furthermore, brands like NIO have expanded their Battery-as-a-Service model across several European countries. With battery-swapping stations increasing in number, NIO has attempted to address the challenge of battery degradation, charging downtime, and resale value. Whether this model becomes mainstream or remains premium-focused, it has added a new competitive angle to the European EV market.

Consumer Psychology: The End of the Budget Label

Surveys conducted in early 2026 show that 65% of European car buyers would consider a Chinese brand for their next purchase, up from just 25% in 2022. The “budget” label has been shed. Today, consumers increasingly associate Chinese cars with advanced tech, modern design, long equipment lists, and strong value. The five-star Euro NCAP safety ratings achieved by many major Chinese exports in recent years have also played a crucial role in building trust.

Internal Market Perspective

For more coverage of Chinese electric vehicles, market reports, and buying guides, visit the Chinese Cars Asia homepage for the latest automotive insights and related articles.

Essential Accessories for Your New Chinese Car

If this report has you seriously considering a Chinese car or EV, a few well-chosen accessories will make ownership smoother from day one—from faster, tidier home charging to interior protection that helps preserve resale value. The items below are practical picks that suit the BYD, MG, NIO, and Xiaomi models discussed throughout this report, rather than gimmicks.

A dual-channel dash cam with a Sony STARVIS sensor and parking mode protects your investment whether you are driving or parked at a charging station. Aim for 4K front / 2K rear with built-in Wi-Fi for easy footage review—increasingly expected by UK and EU insurers and a sound safeguard for a high-value car.

Model-tailored, all-weather TPE floor mats and a boot liner are the single best way to protect interior carpets and preserve resale value—especially relevant for the premium cabins of BYD, MG, and NIO models. Always search your exact model and year to guarantee a precise, no-slip fit.

EVs are heavy, and correct tyre pressure directly affects real-world range and efficiency—a critical factor when WLTP figures already differ from everyday driving. A rechargeable digital inflator with a preset auto-stop keeps pressures optimal and quickly pays for itself in saved range and longer tyre life.

A waterproof, fire-retardant carry bag keeps your Type 2 cable clean and contained in the boot—no more grimy hands or a dirty load space after every charge. A small, inexpensive accessory that solves a daily annoyance every EV owner eventually faces.

Even with the large screens these cars offer, a dedicated MagSafe-compatible mount with wireless charging keeps your phone visible and topped up without cluttering the minimalist dashboards found in Xiaomi, NIO, and BYD cabins. Vent or air-outlet versions fit most interiors cleanly.

Most Chinese EVs in this report use the Type 2 (IEC 62196) standard for AC charging across UK and European networks. A TÜV-certified 32A / 22kW cable future-proofs your setup, reaches awkward public chargers, and works with home wallboxes and street posts alike. A 7m length suits most driveways. Note: this is the European connector, not for the US market, so no US link is shown.

Conclusion: The Road Ahead to 2030

The 2026 report on Chinese car sales in Europe confirms that we are no longer in a period of transition—we are in a new era. The competitive pressure from the East has forced European manufacturers to innovate faster and price more aggressively, which is a net win for consumers.

As we look toward 2030, the synergy between Chinese manufacturing strength and European market requirements will likely define the global standard for mobility. Chinese brands are no longer testing the European market; they are helping reshape it.