Why EV Prices Are Dropping Fast in 2026: The Cost Revolution

Quick answer: EV prices are falling because battery costs have collapsed (down around 85% since 2010), Chinese competition is fierce, manufacturing has reached massive scale, and the supply chain has matured from shortage into oversupply.

By 2030, the average EV is on track to cost roughly 20–30% less than 2026 levels. In this guide we break down the five forces driving the fall — and where prices are likely to land by the end of the decade.

The price of a new electric car in 2026 looks very different from just a few years ago. What began as gradual discounting has turned into a structural repricing of the whole category, driven by cheaper batteries, brutal competition and a maturing supply chain. This is not temporary margin compression — it is a fundamental reset of what an EV should cost.

Before we dig into the numbers, the short explainer below walks through why EV prices are dropping fast in 2026 and where they are heading. We then unpack each driver in detail throughout the rest of the article.

The Price Collapse: By the Numbers

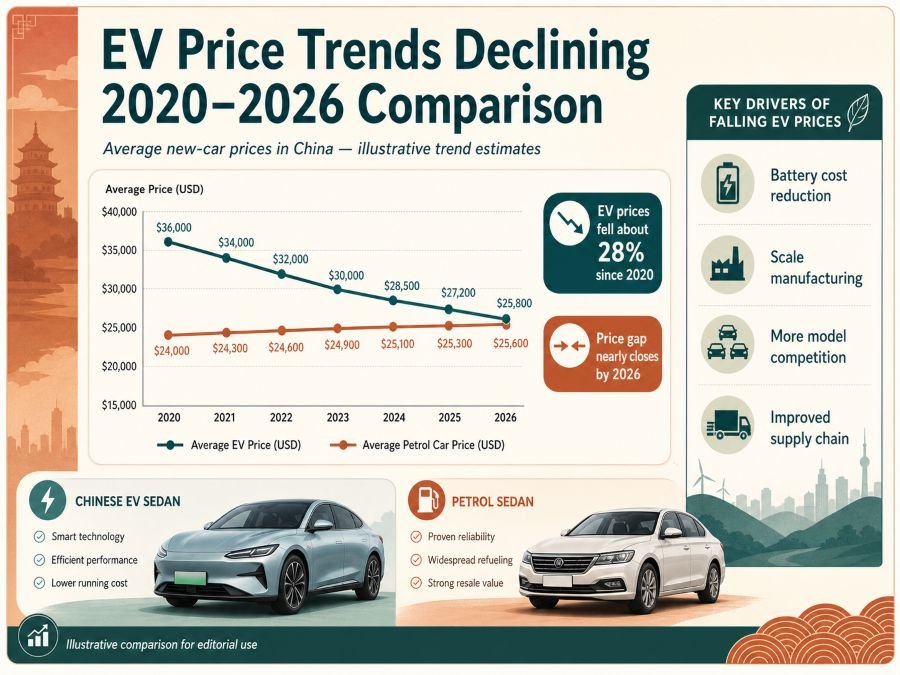

To appreciate how fast EV pricing is moving, it helps to look at the average transaction price after incentives over the past few years. The trajectory is steep and remarkably consistent.

- 2020: Average EV price £35,000–£42,000 (after incentives)

- 2023: Average EV price £28,000–£35,000 (about −20% in three years)

- 2026: Average EV price £22,000–£30,000 (roughly −40% from 2020)

- Projected 2030: Average EV price £16,000–£22,000 (around −50% from 2020)

This is not a one-off promotion or a single brand chasing volume. It is a category-wide repricing that is reshaping how affordable electric mobility has become — and it is being driven by five reinforcing forces.

Protect Your EV’s Value: Two Low-Cost Ownership Essentials

A breathable, waterproof car cover shields paintwork from sun, sap, and grime for owners without garage parking — particularly worthwhile for preserving the finish on a high-value EV. Choose a size band that matches your SUV or sedan’s dimensions.

A quality microfiber towel and detailing set lets you clean paint, glass, and screens safely without swirl marks — protecting the glossy finishes and large displays these cars are known for. An inexpensive kit that pays off at every wash.

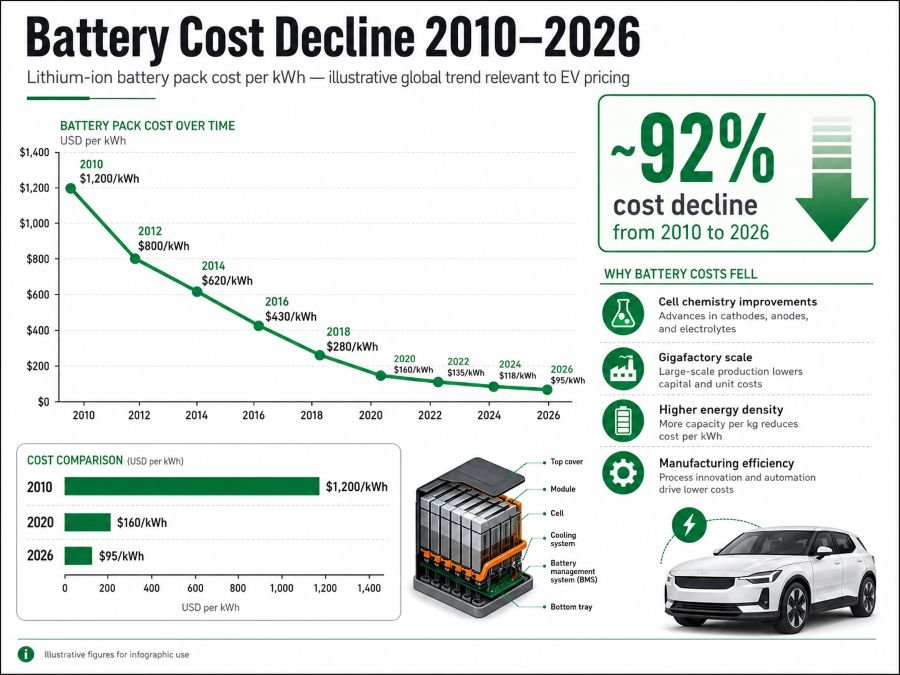

Driver #1: Battery Costs Have Collapsed

The battery is the single most expensive component in an electric car, typically accounting for 30–40% of the total cost. So when battery prices fall, the whole vehicle gets cheaper — and they have fallen further than almost any other major industrial input in modern history.

| Year | Battery Cost (£/kWh) | Year-over-Year Change | Cumulative Decline (vs 2010) |

|---|---|---|---|

| 2010 | £1,100/kWh | Baseline | 0% |

| 2015 | £350/kWh | −68% | −68% |

| 2020 | £130–150/kWh | −60% | −85% |

| 2023 | £90–110/kWh | −30% | −90% |

| 2026 | £60–80/kWh | −40% | −93% |

| 2030 (projected) | £40–50/kWh | −40% | −95% |

The arithmetic is striking. A 60 kWh battery that cost £7,800–£9,000 in 2020 now costs roughly £3,600–£4,800, and a 75 kWh pack lands near £4,500–£6,000. As cell costs approach £50/kWh, EV powertrains start to become cheaper to build than comparable petrol engines and gearboxes — the tipping point the whole industry has been waiting for.

A large part of this decline comes from a shift in battery chemistry. Lithium iron phosphate (LFP) cells, championed by Chinese manufacturers such as BYD with its Blade design, are cheaper to produce than the nickel-rich packs that dominated the early EV years, and they avoid expensive cobalt entirely. As LFP spreads from budget models into the mainstream — and recycling begins to recover materials at scale — the cost floor for a usable battery keeps dropping, pulling entry-level EV prices down with it.

Driver #2: Manufacturing Scale & Efficiency Gains

As production volumes climb, manufacturers ride down the learning curve: fixed costs spread across more units, suppliers compete harder, and factories simply get better at building cars. The volume growth over six years has been extraordinary.

- 2020: around 2.2 million EVs produced globally

- 2023: roughly 10.1 million EVs produced globally

- 2026: an estimated 13–15 million EVs produced annually

- Factory throughput: current lines build 30–50 vehicles per hour, with 75–100 targeted by 2028

- Labour productivity: automation is trimming per-vehicle labour by 3–4% a year

- Supply chain leverage: component suppliers compete aggressively, shaving 2–3% off prices annually

Scale economics are unforgiving in the best possible way for buyers: produce ten times more units and per-unit costs fall dramatically through fixed-cost amortisation and supplier competition. That compounding effect is a major reason sticker prices keep sliding.

Driver #3: Chinese Competition & Price Wars

No factor has reshaped global EV pricing more than competition from Chinese manufacturers, who have used aggressive pricing to win market share at home and abroad. The pressure has forced Western brands to respond, narrowing — but not closing — the gap.

| Vehicle Class | Western Brand (2024) | Chinese Brand (2024) | Gap | Western Brand (2026) | New Gap |

|---|---|---|---|---|---|

| Budget compact | £28,000 | £15,000–£18,000 | −46% | £22,000 | −27% |

| Mid-range sedan | £38,000 | £22,000–£28,000 | −42% | £32,000 | −19% |

| Family SUV | £45,000 | £32,000–£38,000 | −28% | £38,000 | −16% |

Between 2024 and 2026, Western manufacturers were pushed to cut prices by roughly 15–25% to stay competitive — and that pressure shows no sign of easing.

Importantly, this is not simply a story of cheaper cars but of better-equipped ones. Chinese brands typically bundle features that remain optional extras elsewhere — large touchscreens, advanced driver assistance, heat pumps and generous warranties — into their headline price. That forces rivals to compete on value as well as cost, so buyers benefit twice: lower prices and richer standard specifications at the same time.

🔥 Competition effect: Every Chinese price cut forces Western rivals to either trim margins or lower prices in turn. From a consumer’s perspective this is a virtuous cycle, pushing industry-wide pricing down an estimated 3–5% each year.

Driver #4: Supply Chain Maturity & Stabilisation

The early EV era was defined by scarcity, and scarcity always carries a price premium. As the supply chain matured, that premium evaporated — and then flipped into oversupply, which actively pushes prices down.

- 2020–2022: semiconductor shortages, battery constraints and long waiting lists

- 2023–2024: supply normalised and waiting lists largely disappeared

- 2025–2026: battery capacity from giants like CATL and BYD outpaced demand

- Result: suppliers cut prices aggressively to keep their factories running near capacity

The logic is simple: when demand outstrips supply, prices rise; when supply outstrips demand, prices fall. The market has decisively shifted into the second phase.

Driver #5: Incentive Reductions, Offset by Lower Base Prices

Counterintuitively, several governments trimmed EV incentives over 2024–2025 — yet cars still got cheaper, because base prices fell faster than the subsidies were withdrawn.

- UK: the plug-in car grant was reduced from £3,000 to £2,500

- US: the federal tax credit narrowed to fewer vehicles via manufacturing-location rules

- Germany: the environmental bonus was reduced, with a phase-out planned

- Offset: falling vehicle base prices more than compensated for the smaller incentives

The net effect for buyers is positive: even with leaner incentives, EVs are cheaper to purchase today than they were two or three years ago.

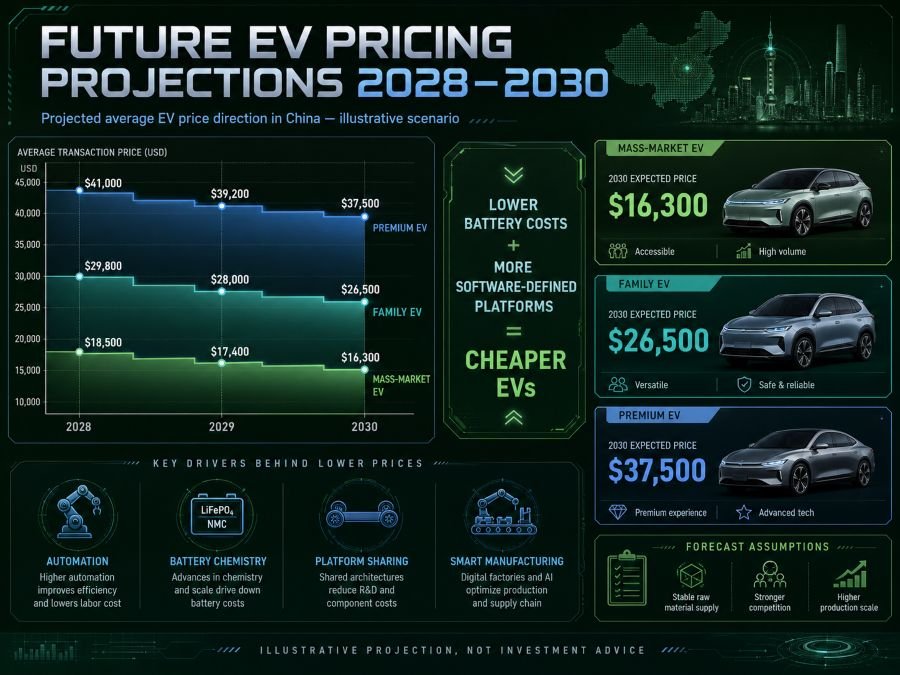

Long-Term Price Trajectory: 2026–2030

Looking ahead, the same forces that have driven prices down are set to keep working. Stacking the major contributors gives a sense of how much further costs could fall by the end of the decade.

| Driver | Impact by 2028–2030 | Vehicle Cost Reduction |

|---|---|---|

| Continued battery cost decline | Solid-state cells and scaling lithium recycling | −8 to −12% |

| Manufacturing automation | Robots and AI reduce labour input | −5 to −8% |

| Component consolidation | Fewer suppliers competing aggressively | −3 to −5% |

| Scale expansion | 25–30 million EVs produced annually | −4 to −6% |

| Total combined impact | Reinforcing effect | −20 to −30% |

Put together, these trends suggest a £22,000 EV today could become a £15,000–£18,000 EV by 2030 — bringing electric cars firmly into the price territory once reserved for budget petrol models.

⚠️ Important note: The 2028–2030 figures here are projections based on current trends. Swings in lithium and other raw-material prices, new tariffs, and shifts in government policy can all alter the trajectory, so treat the longer-term numbers as informed estimates rather than guarantees.

Price Predictions by Vehicle Class (2030)

Breaking the forecast down by segment shows just how accessible electric cars could become within a few years.

- Budget compact (300 km range): £12,000–£15,000 (versus around £22,000 today)

- Mid-range sedan (400 km range): £18,000–£22,000 (versus around £30,000 today)

- Family SUV (500 km range): £25,000–£32,000 (versus around £42,000 today)

- Premium sedan/SUV: £42,000–£52,000 (versus £60,000+ today)

At these levels, the economic case for a new petrol car becomes very hard to defend.

It is worth stressing that range is improving even as prices fall. The budget compacts of 2030 are projected to offer the kind of 300 km real-world range that mid-tier cars struggled to reach only a few years ago, while family SUVs push toward 500 km as standard. In other words, buyers are not trading affordability for capability — they are getting more of both, which is precisely what makes the shift so disruptive to combustion models.

Who Benefits Most from Falling EV Prices?

Cheaper EVs do not just help early adopters — they widen access across the entire market.

- Budget buyers: £15,000 EVs become realistic for working families

- Developing markets: adoption accelerates where affordability is the key barrier

- Used-car buyers: a deeper, cheaper used-EV inventory emerges

- Multi-car households: a second or third EV drops below the cost of an entry petrol car

- The petrol market: faces serious disruption, with fewer reasons to buy new combustion cars

FAQ: EV Prices in 2026

Should I wait to buy an EV until 2030 for lower prices?

No. The fuel and maintenance savings you collect between now and 2030 (roughly £6,000–£10,000) tend to exceed the additional price drop you would gain by waiting. For most buyers it makes sense to buy now and start saving immediately.

Will EV resale values collapse as prices fall?

Gradually, yes, but less than many people expect. Strong demand for affordable used EVs at lower price points helps keep resale values relatively stable even as new-car prices decline.

Will petrol car prices stay high?

Unlikely. Petrol cars are expected to be heavily discounted between 2027 and 2030 as manufacturers clear inventory, and used petrol values are likely to soften as more buyers switch to electric.

Are any EV brands cutting prices faster than others?

Yes. Chinese brands such as BYD, XPeng and NIO are reducing prices most aggressively, while Western brands like Volkswagen, Tesla and BMW are cutting more conservatively to protect premium positioning.

The Price Revolution Is Real — and Accelerating

EV prices are falling in a self-reinforcing loop: lower costs lead to lower prices, which drive higher volume, which lowers costs further still. By 2030, the average new EV is set to undercut the average new petrol car outright — marking the end of combustion’s cost advantage.

If you have been waiting for “cheaper EVs,” many are already here, with Chinese brands offering compelling models in the £15,000–£25,000 range. Based on every major trend, the pace of price reductions looks set to accelerate rather than slow.

The key takeaways are worth keeping in mind: battery costs are down around 85% from 2010 and still falling; global production has multiplied roughly sevenfold since 2020; Chinese competition keeps forcing Western prices lower; oversupply has replaced shortage; and automation continues to trim labour costs. Together they point to EVs costing 20–30% less by 2030, leaving petrol cars increasingly difficult to justify on economics alone.